Technology is changing the way underwriters create submissions. The process is moving from a slow and manual task; to a fast, fully automated, digital process. Now, the data within a submission can be scanned, imported, validated, triaged, and priced automatically, taking a matter of minutes. At scale, this makes the submission workflow extremely efficient. Concirrus’ submissions module now includes the calculation of pricing adequacy as part of this import process, so underwriters can clearly see how attractive business is from the outset.

Determine the quality of business via adequacy

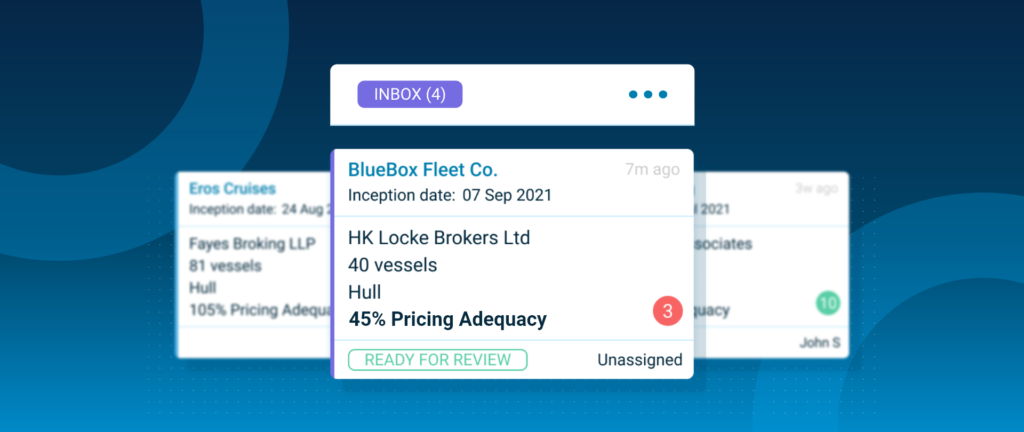

Most underwriters are not permitted to write a risk if it’s price is below a certain pricing adequacy percentage. These rules are set by the organisation and form its ‘appetite’. With pricing adequacy now at the forefront of the submission, an underwriter can immediately filter out submissions that aren’t in appetite. This accelerates the qualification, triage, processing, and response time of the underwriting team, whilst ensuring all new business meets organisational standards.

Fig 1: Pricing adequacy as part of a submissions card in Concirrus’ Submission module

Simply put, if the pricing adequacy of a risk is 45%, it’s unlikely to be bound and therefore warrants no further consideration. The time saves will instead be applied to desirable business, increasing productivity.

Quick and accurate valuations for faster decisions

Adequacy assessments utilise Concirrus’ pricing model to determine an expected loss, which can be calculated using the IMO number alone. Concirrus’ pricing capabilities leverage vast amounts of data to view risk from both a traditional and behavioural perspective. Behaviour is more reflective of risk, and therefore a more accurate assessment of the potential insured. Once the expected loss is calculated, figures such as brokerage, internal expenses, and profit load are added to it. The total sum is then compared to the Annual Gross Premium (AGP) included in most submission rating schedules. AGP shows the premium vessels were previously insured at; or are currently quoted at. This comparison results in the pricing adequacy percentage.

If the risk presented is entirely new business, then adequacy will be calculated upon quotation.

More time spent leveraging underwriting expertise

Fig 2: The broker, risk score, and adequacy help an underwriter decide whether business is desirable

Accelerating the calculation of adequacy for prospective business saves underwriters a lot of time. They can see how business is priced, the score of the risk, and the source in one view. If these values are close to what’s required to be within appetite, an underwriter would have a few options.

- Adequacy: If business is priced close to 100% adequacy, then there’s room for negotiation. Underwriters can decide how much to negotiate depending on risk score.

- Score: If a score is low, then the business has a higher chance of a claim. It may be that if the price is not adequate, and the score is low, then the business is out of appetite. However, this can depend on the source.

- Source: Is the broker favourable? Using the submissions dashboard, an underwriter can check their hit rate and broker list to see which brokers regularly provide high quality business. If the broker in question usually does, then the underwriter may show lenience as they have confidence in the supplier. If not, then the underwriter can pass on the business without compromise.

To find out how submissions can help your business, visit our resource page, or get in touch.