Such evolution calls for a more structured understanding of what ‘autonomous insurance’ truly means. Here, I present my thoughts on a framework that outlines five key stages of the journey, drawing parallels with the autonomous driving sector. Perhaps it’s not the holy grail answer but it certainly would help to foster industry-wide dialogue and consensus. I’ve used examples through this document of both underwriting and claims as I feel that this can apply to both.

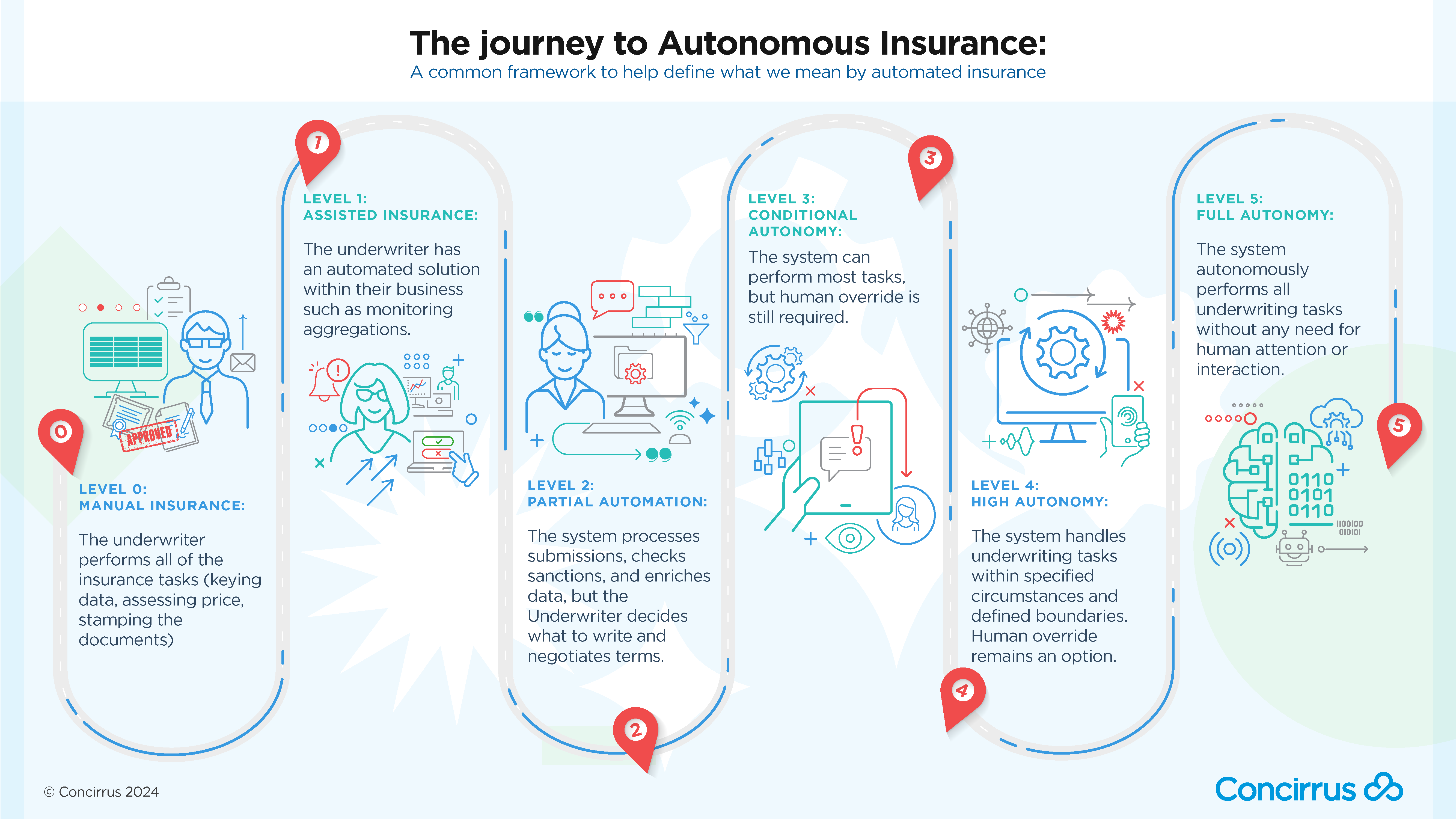

Level 0: Manual Insurance

This is where, for example, the underwriter performs all the insurance tasks (keying data, assessing price, stamping the documents). Traditionally, insurance has been operating at this level with manual decision making where all the knowledge resides ‘in the person’s head’. Systems like Excel may assist underwriters in pricing risks, but they don’t drive the process.

If we consider this in the context of the driving sector, this is centred around manual control. The human performs all driving tasks (steering, acceleration, braking, etc.).

Level 1: Assisted insurance

Within this level, the underwriter/claims manager has an automated solution within their business such as monitoring aggregations or triaging claims. The insurer uses a solution such as sanctions checking and algorithmic pricing for control, but the underwriter still makes decisions on what business to write. For claims, assessment may be assisted by technology to run basic fraud checks or comparable claims, but approval to pay is still done by a person.

The equivalent within autonomous driving would be the vehicle featuring a single automated system (e.g. it monitors speed through cruise control).

Level 2: Partial automation

This is where a system would process submissions, check sanctions, and enrich data, but the underwriter would still decide what to write and negotiate terms. This would often involve an Underwriter Workbench with automated aspects, minimising manual work. Many tasks would be automated using AI, but a human would retain control and can intervene at any time. In claims, this could be a combination of assessment of claims, e.g. using AI to gauge damage to a vehicle and likely repair costs but the negotiation with the assured is still done by a person.

The auto-equivalent would be the vehicle performing steering and acceleration. The human still monitors all tasks and can take control at any time.

Level 3: Conditional autonomy

This level would feature a system that can perform most tasks, but human override is still required. It would be a significant tech shift, but subtle from a user perspective. The system would make informed decisions for itself but would require human override for unmet terms and un-executable tasks.

This could include ‘environmental detection capabilities’ when considering the autonomous driving equivalent i.e. what’s going on around the vehicle, what are other cars doing, etc. The vehicle can perform most driving tasks, but human override is still required. Think of the difference between level 2 and level 3 being that the default ’driver’ in stage 2 is the human with the tech as the co-pilot, whereas in stage 3, these roles are swapped, and the default driver is the AI.

Level 4: High Autonomy

This level of the journey would see a system handling the majority of underwriting/claims processing tasks within specified circumstances and defined boundaries. Human override would remain an option. This may include an automated quote/bind process for follow lines with pre-approved models within set parameters or it may be that claims are processed, validated automatically, and paid. Lemonade’s self-proclaimed one-minute claims process would be an example of this. The system would operate automatically, with the team monitoring risks and anomalies.

Within automotive, this level would be likened to the vehicle performing all driving tasks under specific circumstances e.g. on motorways it could brake, accelerate, change lanes, etc. Geofencing is required to determine when / where is safe to operate autonomously and human override is still an option.

Level 5: Full Autonomy

As you might expect, this level would involve a system that autonomously performs all underwriting and/or claims tasks without any need for human attention or interaction. A fully trained set of AI models that can handle complex risks/claims and can deal with unstructured and structured submissions, contracts, and claims.

The auto-equivalent being a vehicle that performs all driving tasks under all conditions with zero human attention or interaction (and likely no steering wheel or pedals).

It’s important to note the shifting role of decision-making throughout this journey. In levels 0-2, humans remain the primary decision makers with technology playing a supportive role. Conversely, levels 3-5 is where technology takes the lead with humans providing oversight and intervention when necessary.

This journey is exciting but complex and it’s the very reason why a clear framework needs to be established so that we not only understand the current landscape but can pave the way for how we develop in the future. So, let’s engage in meaningful discussions now and set the benchmark so that we can drive towards the ultimate goal of enhancing efficiency, accuracy and customer satisfaction across the insurance market.